Understanding London’s property market can seem overwhelming at first. With its complex zoning system, 33 boroughs, dramatic price variations, especially due to international investment, and the capital’s housing situation being different from anywhere else in the UK, this comprehensive guide outlines everything you need to know about how London property actually works.

Understanding London’s Zone System

London’s zone system originated as a fare structure for Transport for London, but it has evolved into much more than that. Today, zones fundamentally shape property prices, lifestyle choices, and investment decisions across the capital.

What Are London’s Zones?

London is divided into Zones 1 through 6, though the system doesn’t form perfect circles—it follows historical borough boundaries and transport infrastructure. There are also Zones 7-9 extending into the outskirts, covering areas like Watford and Amersham.

Zone 1: Central London

This is the heart of the capital, encompassing Westminster, the City, the West End, and the South Bank. Here you’ll find London’s most iconic landmarks—from Buckingham Palace and Big Ben to the Tower of London. Property prices reflect the area’s exclusivity, with apartments starting at around £5 million and sometimes exceeding £40 million. The average property price in Zone 1 is approximately £1,457,564.

Zone 2: Inner Suburbs

Just outside the city centre, Zone 2 includes desirable areas like Camden, Hammersmith & Fulham, Kensington & Chelsea, Clapham, Shoreditch, and Greenwich. Zone 2 is attractive for property investors thanks to its vibrant neighbourhoods, proximity to central London, and more reasonable property prices than Zone 1, with an average house price of £964,746.

Zone 3: Established Suburbs

Zone 3 covers areas including Wimbledon, Balham, Walthamstow, Leyton, East Ham, and New Cross. Properties here offer approximately 20-30% rent savings compared to Zone 2, with typical one-bedroom flats ranging from £1,200-£1,700 monthly. Zone 3 provides the best space-to-rent ratio in inner London, with Victorian and Edwardian terraces dominating the housing stock.

Zones 4-6: Outer London

These zones extend to the capital’s edge, offering larger homes, more green spaces, and significantly lower prices. Areas like Romford in Zone 6 have average house prices around £423,777, making it budget-friendly for buyers. However, commute times can exceed an hour to central London.

London’s 33 Boroughs Explained

Greater London comprises 32 London boroughs plus the City of London, all created on April 1, 1965, by the London Government Act 1963. Twelve were designated as Inner London boroughs, with the remaining twenty as Outer London boroughs.

Each borough has its own character, demographics, and property market dynamics. Some key points:

- Inner London boroughs tend to be smaller, more densely populated, and generally more expensive

- Outer London boroughs offer more space, family homes, and affordability

- Borough boundaries don’t always align with zones, creating pricing anomalies

- Each borough sets its own council tax rates and provides local services

Prime Central London (PCL) Boroughs

Areas such as Kensington, Chelsea, Westminster, and Camden are most favoured among overseas buyers and have the most non-UK-born residents. These prestigious neighbourhoods command premium prices due to their lifestyle amenities, cultural attractions, and global reputation.

Up-and-Coming Boroughs

As of early 2026, neighbourhoods showing clear gentrification patterns include Peckham (SE15), Deptford (SE8), Walthamstow (E17), and Leyton (E10), where improved amenities and spillover demand are reshaping the market. These areas have seen annual price appreciation of roughly 3-6% in recent years.

Price Differences Across London

London’s property prices vary dramatically depending on location, with some of the UK’s most expensive and most affordable areas existing within the same city.

Current Market Overview

As of early 2026, the average London property price stands around £547,000, with annual growth currently negative at minus 2.4%. This represents a buyer’s market with negotiating opportunities, particularly for flats.

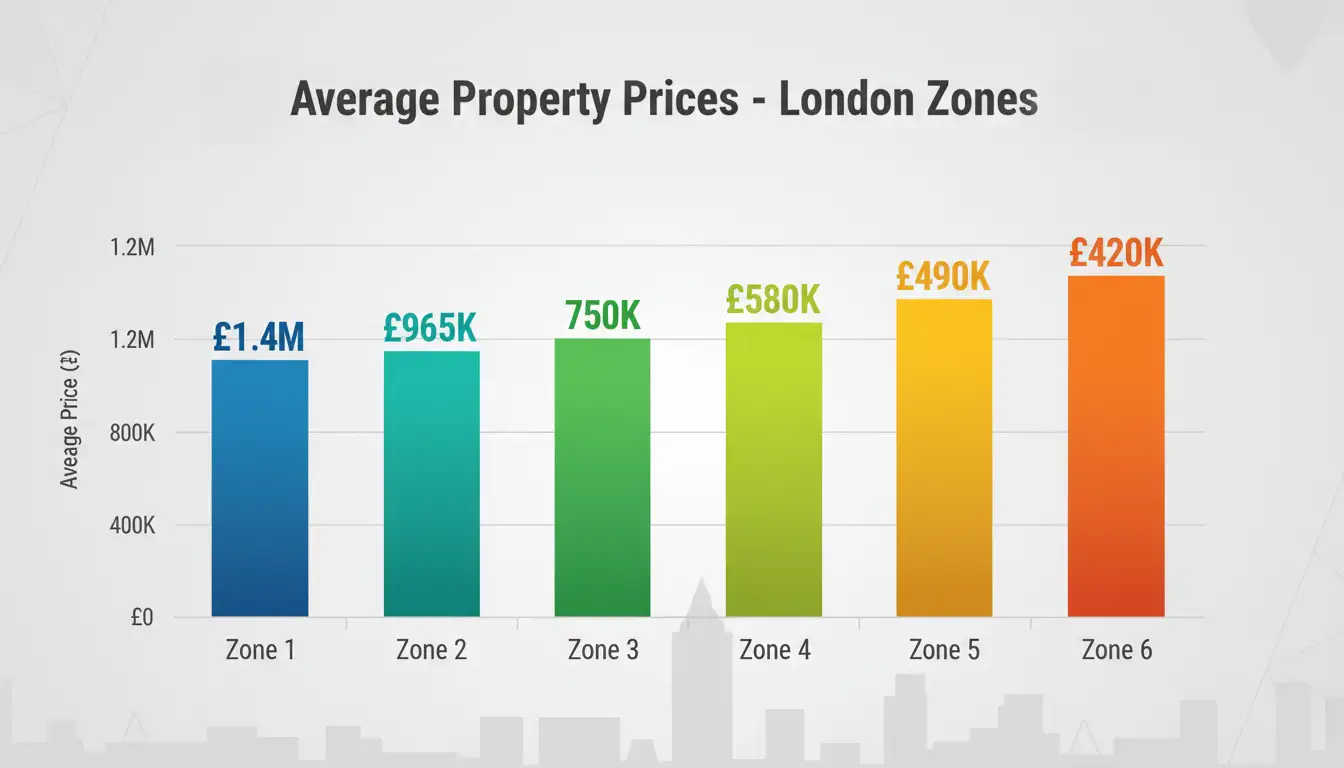

Zone-Based Price Variations

The price gradient from central to outer London is steep:

- Zone 1: £1.4+ million average

- Zone 2: £965,000 average

- Zone 3: 20-30% below Zone 2

- Zone 6: £420,000-£450,000 average

High-Yield vs. High-Value Areas

As of early 2026, London neighbourhoods with the highest gross rental yields include Barking (IG11) at around 6-7%, Woolwich (SE18) at roughly 5.5-6.5%, Stratford (E15) at approximately 5-6%, and Leyton (E10) at similar levels.

Meanwhile, Prime Central London areas deliver lower yields (2.5-3.5%) but offer capital preservation and long-term appreciation potential.

Understanding Property Demand in London

Several factors drive London’s consistently strong property demand:

Population Growth and Housing Shortage

London’s population continues to grow, with demand for housing significantly outstripping supply. This fundamental imbalance keeps pressure on both sales and rental markets, particularly in well-connected areas.

The Rental Market Surge

Average monthly rents across London have reached £2,227, up 11% year-on-year, driven by undersupply, professional relocation, and returning student demand. The rental segment has far outperformed sales in recent years.

Shifting Buyer Priorities

Over half of movers in 2025 relocated within London, most shifting from Zones 1-3 to Zones 4-6, as the balance between affordability and accessibility now defines demand more than prestige. Hybrid working patterns have accelerated this trend, with buyers prioritising space and home offices over central postcodes.

Transport Infrastructure Impact

Transport connectivity remains crucial to demand. The Elizabeth Line has shrunk perceived distance to central London, making outer boroughs feel far less distant. Areas along this new line have seen significant demand increases.

Regeneration Zones

Dagenham and Barking represent one of London’s most significant growth frontiers, undergoing colossal transformation with extensive state-backed regeneration. Other major regeneration areas include Canning Town (£3.7 billion investment), Old Oak Common, and the Old Kent Road corridor.

The Role of Overseas Buyers

International investment plays a significant and influential role in shaping London’s property market, particularly in prime areas.

Scale of Foreign Investment

Almost 27% of total London properties sold in Q1 2024 were acquired by foreign buyers, with ownership of London properties worth over £90 billion. Recent research shows foreign homeowners accounted for approximately 190,000 properties in England and Wales in 2024, representing a 2.6% increase year-on-year.

Who’s Buying?

Hong Kong-based buyers were the largest contingent of overseas homebuyers in 2024 with over 13.5% of the share, followed by buyers from Singapore (8.2%), USA (6.4%), UAE (5.4%), China (5.2%) and Malaysia (5.1%).

The British Nationals Overseas (BNO) Visa launched in 2021, has significantly increased Hong Kong buyer activity, with a 5.7% year-on-year increase. Similarly, there was a 5.5% increase in US buyers and a 12.9% rise in Chinese buyers.

What Drives International Investment?

Several factors make London attractive to overseas buyers:

1. Legal Transparency and Ownership Rights The UK has no restrictions on foreign property ownership, offering international buyers the same access as UK residents. The legal system provides strong buyer protections and transparent transaction processes.

2. Economic and Political Stability London’s resilience through economic crises, Brexit, and the pandemic reinforces its reputation as a haven for capital preservation.

3. Education and Employment London’s world-class universities (Imperial College, UCL, King’s College, LSE) attract international students whose parents often purchase property. The city’s position as a global financial and business hub also draws overseas professionals.

4. Rental Income Potential Almost 70% of overseas property buyers, mainly from Asia and the Middle East, invest to benefit from the UK capital’s thriving rental sector. Typical rental yields range from 3-5% in central areas to 5-7% in outer boroughs.

5. Currency Advantages Currency fluctuations can significantly impact purchasing power for international buyers, making London property more or less attractive depending on exchange rate movements.

Tax Implications for Foreign Buyers

As of April 2025, overseas buyers are subject to Stamp Duty Land Tax (SDLT), which typically includes a 2% surcharge for non-UK residents, in addition to the standard rates, which include a 5% higher rate for additional properties.

Geographic Preferences

Prime Central London areas such as Kensington, Chelsea, Westminster, and Camden are most favoured among overseas buyers. However, as prices in PCL remain elevated, foreign investors increasingly look to Zone 2 and outer boroughs, including Southall, Hayes, West Ham, Woolwich, and Wandsworth, where regeneration projects offer strong growth potential.

Market Impact

According to a London School of Economics study, for every 1% increase in the share of residential transactions to foreign entities, the market witnesses a 2.1% increase in house prices. This demonstrates the significant price influence of international capital flows.

Changing Investment Patterns

Recent data reveals an important shift: for every absentee foreign investor, there are now 2.7 foreign buyers planning to relocate to the UK, suggesting overseas investors are increasingly buying with long-term relocation plans rather than purely for investment purposes.

2026 Market Outlook

Looking ahead, several trends are shaping London’s property market:

Price Forecasts

Savills forecasts approximately 4% growth in 2026 and 15% over five years, while Knight Frank predicts 18% growth over the same period. Outer and mid-priced boroughs like Richmond, Walthamstow, and Enfield are expected to outperform as affordability drives demand.

Interest Rate Environment

Following aggressive rate hikes in 2023-2024, the Bank of England has begun easing monetary policy. This shift is improving mortgage affordability, particularly for first-time buyers and investors in outer boroughs.

Rental Market Outlook

With demand still significantly outpacing supply, rents are expected to remain elevated. However, growth rates may moderate from the double-digit increases seen in recent years.

Key Investment Areas

Growth will likely be led by outer boroughs benefiting from infrastructure improvements, regeneration schemes, and relative affordability. Areas along the Elizabeth Line and other transport upgrades continue to see strong interest.

Practical Tips for Navigating the London Market

Whether you’re a first-time buyer, investor, or overseas purchaser, these insights will help:

- Research transport links carefully: Proximity to Tube, Overground, and especially the Elizabeth Line significantly impacts property values and rental demand.

- Look beyond zone numbers: Some Zone 3 and 4 areas (like Richmond and parts of Ealing) are wealthier and more desirable than some Zone 1-2 locations.

- Consider regeneration timelines: Properties in regeneration zones offer growth potential, but development can take 5-10+ years to fully materialise.

- Understand rental yields vs. capital growth: Prime central areas offer stability and appreciation but lower yields, while outer boroughs provide higher rental returns but potentially higher volatility.

- Factor in all costs: Beyond purchase price, consider Stamp Duty (including foreign buyer surcharges if applicable), legal fees, survey costs, and ongoing expenses like service charges and ground rent.

- Work with local experts: The London market is highly localised. Estate agents, solicitors, and property managers with area-specific expertise are invaluable.

- Be patient in negotiations: With prices down 2.4% year-on-year and the average time to secure a buyer around 63 days, buyers have room to negotiate.

Final Thoughts

London’s property market is complex, dynamic, and deeply segmented by geography, price point, and buyer type. The zone and borough system creates distinct micro-markets, each with its own character, pricing, and investment potential.

For 2026, the market presents opportunities for informed buyers. Prices have stabilised after recent declines, mortgage rates are easing, and outer boroughs offer compelling value for those willing to trade postcode prestige for space and affordability.

Whether you’re looking for a family home, a buy-to-let investment, or a pied-à-terre in the global capital, understanding these fundamental market dynamics will help you make confident, informed decisions in London’s fascinating property landscape.

Disclaimer: Property markets fluctuate, and forecasts are subject to change based on economic conditions. This guide provides general information and should not be considered financial or investment advice. Always consult with qualified professionals before making property decisions.

Join The Discussion